[ad_1]

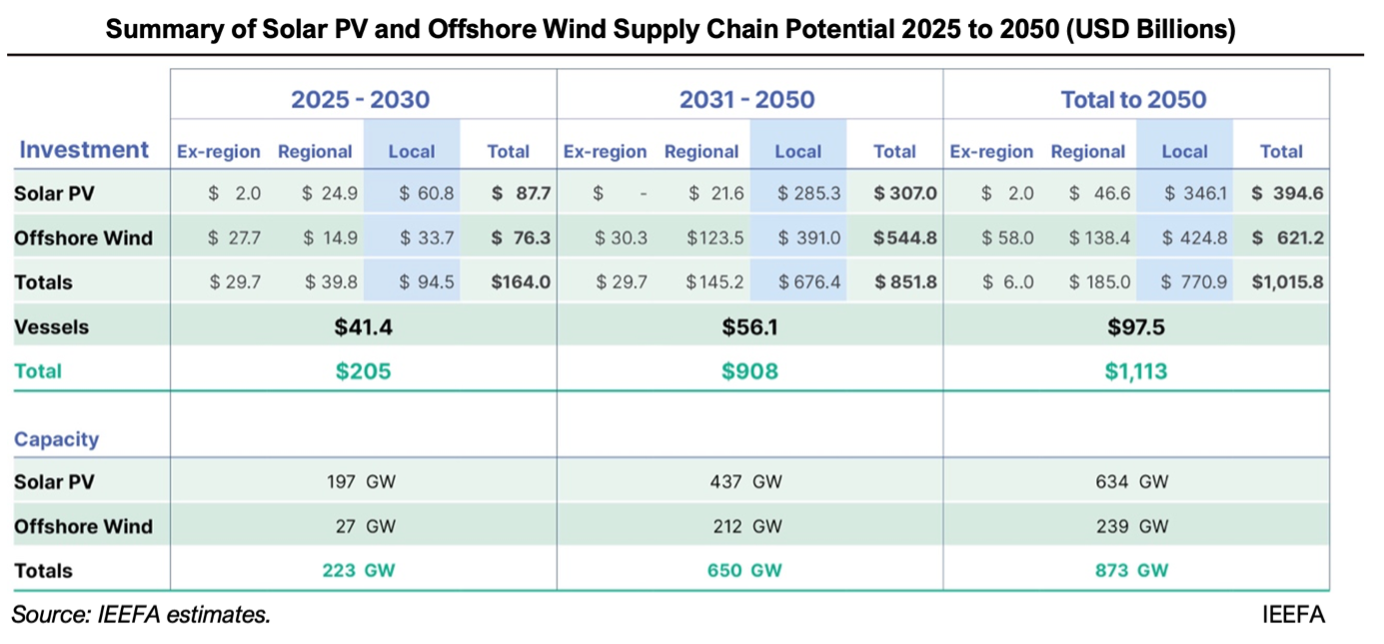

June 27, 2024 (IEEFA Matter): The funding potential for photo voltaic and offshore wind energy challenge provide chains has exceeded US$1.1 trillion by 2050, with inventive capability 873 gigawatts (GW) of fresh power, in line with a brand new report from the Institute for Energy Economics and Financial Analysis (IEEFA).

“This report highlights the here-and-now alternative to capitalize on the renewable power provide chain,” stated Grant Hauber, IEEFA’s Strategic Energy Finance Advisor, Asia. “Solar power presents fast funding advantages within the Asia Pacific, whereas the benefits of becoming a member of the onshore wind provide chain will develop over the following few years.”

The report focuses on seven Asian markets: Japan, South Korea, Malaysia, Taiwan, Vietnam, the Philippines, and Indonesia. IEEFA estimates that by 2050, photo voltaic PV plans purpose to achieve 634 GW of capability, requiring an funding of US$ 394 billion, with US$ 346 billion of that quantity probably will probably be spent on native provide chains. Offshore wind represents a US$621 billion alternative to ship 239 GW of capability, with US$425 billion anticipated to be localized.

In addition, there is a chance within the maritime sector price US$72 to US$97 billion to construct offshore wind installations and repair vessels, with virtually all of this funding anticipated to return from the area.

“The report maps every component of the challenge’s provide chain, quantifies the potential for capital funding, and goals to encourage extra formidable and long-term insurance policies, which is able to assist buyers and policymakers recognize the magnitude of the chance,” stated Hauber.

Looking ahead to the panels and generatorss

In addition to the promise of low power prices, there are alternatives to localize giant proportions of the photo voltaic and offshore wind provide chains required for totally operational energy technology initiatives.

“An necessary message for coverage makers and industrialists is that you just need not construct photo voltaic PV modules or wind generators to understand large-scale home manufacturing and funding advantages,” stated Hauber.

According to the report, non-panel and non-turbine spending will account for at the least 75% of complete funding till 2050, representing a $770 billion alternative for home industries over the following 25 years. .

“There are supplies, elements, infrastructure, logistics, and companies that may present important worth to the home economic system over sustained durations and might be traded regionally and past,” Hauber stated.

China presently dominates the worldwide provide chain for photo voltaic PV panel manufacturing, supplying practically 85% of world demand at prices which are unlikely to be matched for at the least the remainder of the last decade.. Outside of China, as an alternative of manufacturing PV modules, nations can direct home funding to different project-level elements that make up accomplished photo voltaic farms.

Hauber advocates the idea of steadiness of system (BOS), which covers all prices and elements past the photo voltaic panel. IEEFA estimates that BOS investments make up the vast majority of PV farm prices, which, relying available on the market, vary from 55% to 75% of complete challenge prices.

“Within the photo voltaic PV challenge provide chain, virtually all the challenge growth and financing prices are incurred domestically and probably half or extra of the BOS prices might be sourced domestically,” Hauber stated. .

Meanwhile, Asia’s offshore wind assets are considerable, prime quality, and predictable. The area’s conventional maritime economic system has inherent benefits in shipbuilding, steelmaking, marine upkeep, and offshore companies, making them well-suited for large-scale offshore wind initiatives.

“The wind power capability obtainable in virtually each nation within the Asia Pacific is larger than their present complete put in capability from all sources of technology,” stated Hauber. “Wind farms have develop into aggressive sufficient to undercut imported pure gasoline and coal, even in markets the place costs are backed and within the absence of carbon pricing.”

Shipbuilding for offshore wind presents a standalone alternative price as much as US$97 billion, with most of that funding required within the close to time period. Hauber emphasised that world wind service fleet additions haven’t saved tempo with the rising measurement of generators and the rising scale of wind farms.

The world push for offshore wind farms is creating many alternatives for shipyards throughout the Asia Pacific to fulfill this rising demand. Currently, there are a restricted variety of area of interest shipyards that construct these ships, principally in Norway and China. There is a selected want for particular wind turbine set up vessels, as just a few can set up the biggest, next-generation generators.

Currently, solely about 20% of wind farm inputs are of native origin within the area, however with continued demand, this might develop to between 66% and 80% of the full funding quantity. Hauber steered that the mixed offshore wind farm and particular ship market represents an funding alternative of round US$ 878 billion till 2050.

Untapped potential

The report focuses on presently introduced capability targets for photo voltaic and offshore wind, however the market potential might be even higher.

If the capital prices for photo voltaic PV and offshore wind proceed to fall as predicted, these applied sciences will provide the bottom degree electrical energy prices on each nationwide grid. With such enticing power prices, capability targets are more likely to increase to seize the financial advantages.

At current, most nations within the Asia Pacific appear to be underestimating this chance. The report highlights that, regardless of virtually each nation within the area having world-class photo voltaic and wind assets, deliberate renewable capability additions stay a restricted share of electrical energy provide.

For instance, Indonesia has one of many smallest photo voltaic bases in Asia, with the least aggressive additions relative to its obtainable assets. Japan, regardless of having top-of-the-line wind assets on this planet, has very modest offshore wind program targets, aiming for lower than 5% of complete demand in 2050.

According to Hauber, coverage alignment is required now to assist nations understand this potential. Focusing on maximizing low-cost capability additions at scale will create recurring demand, permitting native industries to benefit from photo voltaic and offshore wind provide chains.

“Ultimately, native companies profit from larger quantity development, shoppers profit from decrease long-term electrical energy prices, and the federal government advantages from these positive factors and important enhancements in direction of the decarbonization targets,” stated Hauber.

Read the report: The Asia Pacific Renewable Supply Chain Opportunity

Read the factsheet: Race for trillion-dollar renewable funding alternatives in Asia Pacific

Contact the creator: Grant Hauber ([email protected])

Media contact: Alex Yu ([email protected])

About IEEFA:

The Institute for Energy Economics and Financial Analysis (IEEFA) examines points associated to power markets, developments and insurance policies. The Institute’s mission is to speed up the transition to a various, sustainable and worthwhile power economic system. (www.ieefa.org)

[ad_2]

Source link

{kind=link}