[ad_1]

About 60% of California power clients incorporate battery power storage into their rooftop photo voltaic installations. However, a “continued decline” is predicted for the market.

From pv journal USA

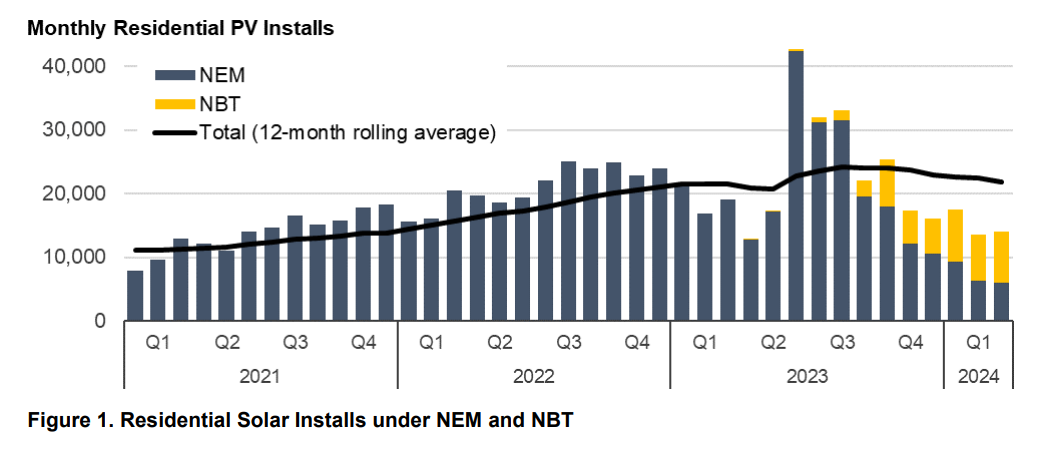

California transitioned its rooftop photo voltaic coverage on April 15, 2023, eliminating web power metering (NEM) and shifting to a net-billing tariff (NBT) construction. The change cuts the speed paid to clients for exporting their extra photo voltaic manufacturing to the grid by about 80%. A 12 months in the past, the Lawerence Berkeley National Laboratory (LNBL) launched a report evaluating adjustments within the state’s rooftop photo voltaic market.

LNBL discovered that rooftop photo voltaic installations in California might be roughly the identical from 2023 to 2022. However, 80% of the methods put in are NEM 2.0 installations that rush into the interconnection queue earlier than the April 15, 2023 deadline. to make sure a extra worthwhile charge construction. To date, about 50,000 methods have been related below the brand new NBT construction, along with the 200,000 NEM methods related on the identical time.

The knowledge comes from EnergySage, operator of the most important residential photo voltaic quote web site within the United States, “suggesting a extra sustained decline,” the report mentioned.

Quote requests peaked throughout the December 2022-April 2023 window between the announcement and implementation of the NBT. Since then, month-to-month quote requests have averaged almost 60% of historic ranges (2019-21).

The 40% drop in historic quote requests is a “main indicator” for market exercise and “maybe the clearest sign of a big and persevering with market decline,” LNBL mentioned. .

A major decline within the rooftop photo voltaic market isn’t an excellent end result for California, a state with bold clear power targets and an electrical energy affordability disaster. Trade affiliation leaders warned that California unlikely to fulfill its clear power targets no sturdy contribution from the rooftop photo voltaic business.

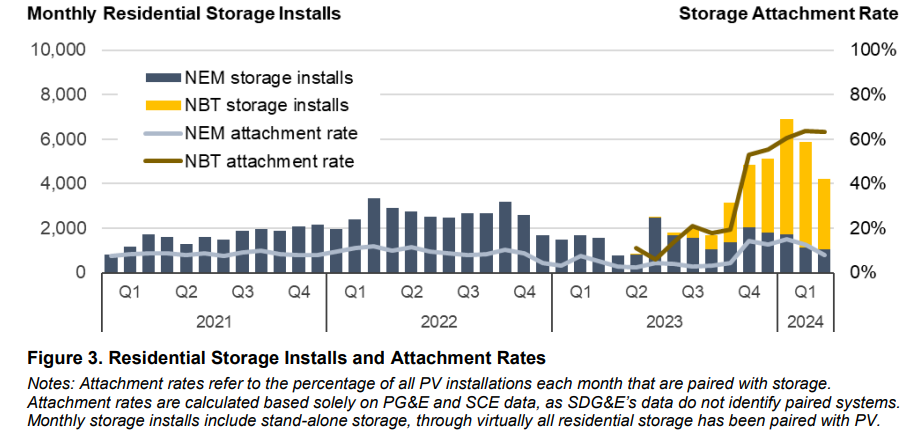

However, the NBT transition has produced some fascinating leads to California. The profile of an put in system has modified considerably. Pre-NBT, clients included battery power storage of their rooftop array in roughly 10% of installations. Today, post-NBT installations embody batteries 60% of the time.

This is vital for California grid operators, who need to clean out the mismatch between solar-generated electrical energy provide and grid wants. This mismatch, often represented by “duck curve“is deepening in California, inflicting pricing and grid upkeep points, and creating a necessity for inefficient pure gasoline “peaker” vegetation to serve intervals of excessive demand and low technology.

The excessive battery attachment charge affords clients some advantages, too. While the general sticker value will increase with a battery-attached system, the return on funding will increase relative to a solar-only set up.

Installers report the median payback interval which is eight years for photo voltaic methods with batteries, whereas standalone photo voltaic methods have an extended median payback interval of about 10 years. Battery storage allows clients to retailer their photo voltaic manufacturing and use it when grid costs are at their peak, as a substitute of promoting it to the grid for pennies on the greenback on sunny afternoons. Solar-battery homeowners even have the choice to be cpaid for exporting energy throughout peak demand occasions or emergenciesprobably creating a brand new income stream.

Customers with batteries additionally profit from having backup energy throughout grid outages, which stays the primary cause for putting in batteries nationwide, based on an installer survey through SolarOpinions.

“As of November 2023, house storage installations are averaging almost 5,000 methods monthly, greater than double the month-to-month tempo of the earlier three years,” mentioned a report from LNBL.

The Berkeley Labs report famous a shift in financing choices for residential photo voltaic clients. Over the final 12 months within the NEM, third-party possession charges, together with leased and energy buy settlement methods, averaged 26% for stand-alone photo voltaic and 11% for in photo voltaic and storage methods. It jumped to 39% for standalone photo voltaic and 52% for photo voltaic plus storage below the NBT system. Some of this alteration could also be on account of rising rates of interest mortgage phrases for purchasers who’re harder to digest.

Finally, the Berkeley Labs report notes elevated consolidation within the California rooftop photo voltaic market. The market share of the highest 5 installers within the state elevated from 40% final 12 months in NEM to 51% within the first 12 months of NBT.

One 12 months in, it is clear that the NBT change is dramatically altering the California rooftop photo voltaic business. However, the backlog of NEM orders to be served in 2023 makes it unclear what the general affect of this coverage change might be. This units the stage for 2024 to be a crucial testomony to the well being of this business.

“These tendencies, and others, will undoubtedly come into sharp focus within the subsequent 12 months or so, as soon as the NEM backlog is totally cleared and a ‘new regular’ below NBT set in,” concluded Galen Barbose, workers scientist, LNBL.

This content material is protected by copyright and might not be reused. If you wish to cooperate with us and wish to reuse a few of our content material, please contact: [email protected].

[ad_2]

Source link

{kind=link}